A Study of the Functionally Effective Credit Lending Models of Microfinance

A Study of the Functionally Effective Credit Lending Models of Microfinance

Sanjay Sinha/Volume 13/Issue 2/(April-September 2020)

ABSTRACT

Microfinance means transaction of financial services with small amount of capital. In past three decades microfinance has emerged as a high impact tool of financial inclusion thereby promoting inclusive growth. All the governments across the globe broadly have the same objective of moving towards inclusive growth and microfinance is seen as a tool that can fulfill this objective beyond a mere financial instrument. Microfinance has varied products like microcredit, micro-insurance, micro-savings and many more. The success of Grameen Bank of Bangladesh founded Prof Mohammed Younus is an excellent example of turnaround that microcredit can bring in the lives of millions of people who are at the bottom of economic pyramid. The method of funds disbursal of microcredit as adopted by Prof Mohammed Younus led to the formation of Grameen Bank in Bangladesh. It has been observed that microcredit assists capacity building of beneficiaries and acts as an instrument directed towards eradication of poverty. However, effectiveness of credit disbursals and economic progress largely depends upon the method adopted by financial institutions in disbursal of funds. Credit Lending Models that are functional at ground level have evolved in course of time based upon local socio-economic and cultural traits prevalent in a particular geographical location. Further, it has been observed that there is multitude of credit lending model across cultural landscapes. The existence of myriad credit lending model leads to overlapping of their features and difficult to understand by practitioners and academicians. This research paper attempts to bring these credit lending models on one platform. The objective of this research paper is two pronged first, compilation of various operational credit lending models and second, classification and description of features of these credit lending models. In order to fulfill the above two objectives of this research, detailed study has been conducted by visiting microfinance beneficiaries, attending meeting of institutional representatives with beneficiaries, discussion with practitioners, experts of microfinance, regulators and academicians. The secondary sources of data have been gathered through magazines, journals, articles and various websites. The outcome of this comprehensive study is detailed enlisting and describing features of operational and effective models of microfinance. The research is descriptive in nature as it compiles various operational models in a theoretical framework for academic understanding and learning.

Keywords: Microfinance, Credit Lending, Financial Inclusion, Capacity Building

1.0 INTRODUCTION

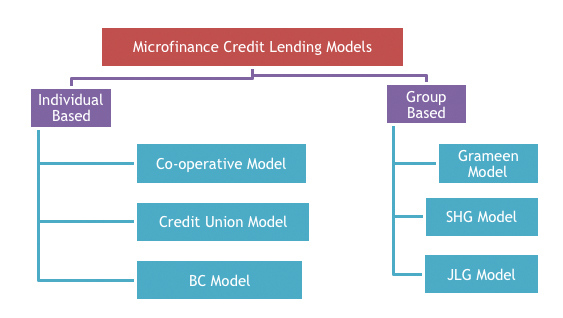

There are multitudes of credit disbursals models that are used for providing financial services in the domain of microfinance. The credit lending models of lending models, the financial services are provided to economically poor people as individuals while in group credit lending model provided to economically poor people as microfinance are broadly divided

into two categories – Individual lending models and Group lending models. In individual credit models, the formation of group is essential for the disbursal of credit. The Individual lending models are generally adopted by both institutional and non-institutional players. Among the institutional sources, banks are mostly using individual models. The group IJBIT/ISSN 0974-5874/V13/02/267/RP A Study of the Functionally Effective Credit Lending Models of

Microfinance Sanjay Sinha

ABSTRACT Microfinance means transaction of financial services with small amount of capital. In past three decades microfinance has emerged as a high impact tool of financial inclusion thereby promoting inclusive growth. All the governments across the globe broadly have the same objective of moving towards inclusive growth and microfinance is seen as a tool that can fulfill this objective beyond a mere financial instrument. Microfinance has varied products like microcredit, micro-insurance, micro-savings and many more. The success of Grameen Bank of Bangladesh founded Prof Mohammed Younus is an excellent example of turnaround that microcredit can bring in the lives of millions of people who are at the bottom of economic pyramid. The method of funds disbursal of microcredit as adopted by Prof Mohammed Younus led to the formation of Grameen Bank in Bangladesh. It has been observed that microcredit assists capacity building of beneficiaries and acts as an instrument directed towards eradication of poverty. However, effectiveness of credit disbursals and economic progress largely depends upon the method adopted by financial institutions in disbursal of funds. Credit Lending Models that are functional at ground level have evolved in course of time based upon local socio- economic and cultural traits prevalent in a particular geographical location. Further, it has been observed that there is multitude of credit lending model across cultural landscapes. The existence of myriad credit lending model leads to overlapping of their features and difficult to understand by practitioners and academicians. This research paper attempts to bring these credit lending models on one platform. The objective of this research paper is two pronged first, compilation of various operational credit lending models and second, classification and description of features of these credit lending models. In order to fulfill the above two objectives of this research, detailed study has been conducted by visiting microfinance beneficiaries, attending meeting of institutional representatives with beneficiaries, discussion with practitioners, experts of microfinance, regulators and academicians. The secondary sources of data have been gathered through magazines, journals, articles and various websites. The outcome of this comprehensive study is detailed enlisting and describing features of operational and effective models of microfinance. The research is descriptive in nature as it compiles various operational models in a theoretical framework for academic understanding and learning. Keywords: Microfinance, Credit Lending, Financial Inclusion, Capacity Building

1. Sanjay Sinha, HoD Finance, ITM Business School, Navi Mumbai

International Journal of Business Insights and Transformation ISSN 0974-5874 Volume 13, Issue 2, April-September 2020

2. models are very popular form of credit disbursal adopted by SHGs, JLGs, MFIs and other financial institutions. The non- institutional sources in general does not adopt group lending models. Both these models have their relative advantages and disadvantages however, all the credit lending models do use peer pressure as a most important collateral in place of physical form of collateral.

The Figure1 above shows that credit lending models can broadly be classified in two distinct categories viz. individual models and group models. There are two secondary models known as technological and new business or emerging models. Some of the popular models are Association Model, Community Banking Model, Cooperative Model, Credit Union Model, Grameen JLG Model, SHG Model, Rotating Saving and Credit Association Model, NGO Model and Village Banking Model. The empirical studies conducted by the researcher has led to the conclusion that credit lending models which are currently used by MFIs are fusion of two or even more than two credit lending models. Accordingly,

their transactional features are also amalgamated version of few of these slackly joined models. It has been further observed that the majority of the credit lending models have evolved in the course of time and they are now structured models of the erstwhile locally operational credit disbursal methods. These indigenous models are still popular in rural areas as a source of informal credit lending especially where banking and other formal institutions are still not present.

2.0 OBJECTIVES

Microfinance refers to the provision of financial services which are in small amounts of money. The term ‘micro’ is used to denote ‘small amount’ and ‘finance’ is used to mean ‘money’. Hence amalgamation of these two words leads to denote an additional segment of finance wherein the transactions carried out are in small monetary values. In past three decades microfinance has emerged as a high impact factor instrument to bring about the financial inclusion. It has been further observed that higher is the financial inclusion the more is the inclusive growth. At the global level, there are many examples of governments promoting microfinance to move towards the goal of achievement of

inclusive growth for the citizens of their countries. Thus, broadly speaking nations have the same objective of progressing towards inclusive growth and microfinance is seen as a tool that can fulfill this objective beyond a mere financial instrument. Further, it has been observed that microcredit assists capacity building of beneficiaries and acts as an instrument directed towards eradication of poverty. However, effectiveness of credit disbursals and economic progress largely depends upon the method adopted by financial institutions in disbursal of funds. Credit lending models that are functional at ground level have evolved in course of time based upon local socio- economic and cultural traits prevalent in a particular geographical location. In the context of developmental economics adopted by the nations there are multiplicity of strategies under the fiscal policies wherein credit lending is carried out through various methods across cultural landscapes. The existence of myriad credit lending models leads to overlapping of their features and difficult to understand by practitioners and academicians. This research paper attempts to bring various credit lending models on one platform. The objective of this research paper is two pronged first, compilation of various operational credit lending models and second, classification and description of features of these credit lending models. The outcome of this comprehensive study is detailed enlisting and describing features of operational and effective models of microfinance. The research is descriptive in nature as it compiles various operational models in a theoretical framework for academic understanding and learning.

3.0 LITERATURE REVIEW

Microfinance transactions include various financial services beyond credit lending. It includes remittances, micro-insurance, micro- savings, insurance mutual and others. The

credit lending activities inter-alia are the mostly widespread across all regions where microfinance operations remains in place. The credit lending methods practiced in different regions and by different agencies have significant variations. According to the Global Development Research Center, Microfinance institutions are the oldest financial institutions in the world, but with time they have adapted to the changes, and have started using various credit lending models. Microfinance services are provided with different methods in India. A total of 14 models are existing in India. They include associations, bank guarantees, community banking, cooperatives, credit unions, Grameen, group, individual, intermediaries, NGOs, peer pressure, ROSCAs, small business, and village banking models. In reality, the models are loosely related with each other, and most good and sustainable microfinance institutions have features of two or more models in their activities. The Microfinance lending models vary in their legal forms, in the channels and methods of delivery, in their governance structure, in their approach to sustainability and also in their approach to microfinance where their funds are sourced from, and how the money is governed [United Nations, Global Development Research Center, www.gdrc.org, 2015] Another research states that microfinance itself is a credit lending model, and within this lending model exist several sub-categories, i.e. microfinance lending models, which differ in terms of where their funds are sourced from, and how the money is governed. It is further stated that there are 8 microfinance lending models [Microfinance-Lending- Models, scribd.com/document, 2016]. According to Arthapedia, the four most important Micro Finance models prevalent in India are: Model I - individuals or group borrowers are financed directly by banks without the intervention/facilitation of any Non- Government Organisation (NGO). Model II - borrowers are financed directly with the facilitation extended by formal or informal agencies like Government, Commercial Banks and Micro-Finance Institutions (MFIs) like NGOs, Non-Bank Financial Intermediaries and Co-operative Societies; Model III - financing takes place through NGOs and MFIs as facilitators and financing agencies; Model IV - is the Grameen Bank Model, similar to the model followed in Bangladesh. In India, Model II of MF constitutes three- fourths of total micro-financing where activity/joint liability/Self-Help Groups are formed and nurtured by facilitating agencies and are linked directly with banks for the purpose of receiving credit [Arthapedia – a portal by government economists of India known as Indian Economic Services, http://www.arthapedia.in]. The literature survey shows that the approach adopted by different researchers and institutions have defined the various credit lending models prevalent differently. It can be further said that there is no consensus on the number of credit lending models because there are overlapping of features of these models and two or more models can have few features similar while other features can be divergent. This research to fulfill its objective of bringing all models on a single platform so that they can be studied together has primarily considered the features of these models as differentiating factor. The following paragraphs contains detailed discussion on various credit lending models which are in practice by various formal and non-formal institutions operating the domain of microfinance:

4.0 INDIVIDUAL MODEL

Individual models are the simplest among all the credit lending models. In the individual

model microloans or microcredit is provided to the borrower. This model does not necessitate formation of groups for the application of peer pressure towards repayment of loans. This model is mostly practiced by banks and the beneficiary is solely responsible for timely repayment of loan. The other players of microfinance industry like SHGs, JLGs, MFI does not practice this model. The individual model adopts comprehensive approach as it incorporates microfinance services beyond credit lending. These models in addition to credit disbursals include functions like socio-economic services for skill development, education, and other outreach services for the beneficiaries. There are many Individual models of Credit Lending however few of the functional models viz. cooperative model, credit union model and BC model have been discussed in the next paragraphs. 4.1 Cooperative Model In this model of credit disbursement, the individuals form a group known as cooperative. The cooperative essentially remains an autonomous association of group of people. The people forming the group are members of the cooperative. The members of the group pool their resources and they join together voluntarily to meet their common socio-economic and cultural needs. A cooperative remains a democratic cooperative which is run by its members. Few cooperatives carry out savings and financing activities for its members. These types of cooperatives are known as financial cooperatives.

Few of important features of these financial cooperatives are:

- members are economically poor and belong to lower- and middle-income group

- these financial cooperatives have their own capital which is raised by the members. They do not borrow funds from outside agencies

- the financial services are provided only to the members of the cooperative. The lending in this model is very simple. Credit is disbursed directly to beneficiary and repayment obligation remains confined to individual.

- Interest is neither paid on the deposits nor it is charged on the loans. Credit is given to individuals which is repaid in series of installment, usually interest free

- they do not have professional managers rather the members of the cooperative manage all the activities pertaining to these financial cooperatives.

- meetings are regularly conducted; members mostly know each other, and they share similar socio-economic background

- they act as self-regulatory organizations

These types of cooperatives have many forms in India. Few of these cooperatives are farmers cooperatives, consumer cooperatives, cooperative housing societies, building cooperatives, retailers’ cooperatives, social cooperatives, agricultural cooperatives and many more. The members are people having some common bond like working in the same organization or labour union or social fraternity or living in the same community. Membership remains open to anyone belonging to the group regardless of race, religion, colour or creed.

4.2 Credit Union Model Credit

Union Model is a variation of cooperative model in the sense that Credit Unions have primary objective is channelization of funds while in cooperative model the primary objective remains achievement of common socio-economic and cultural needs. Credit Unions are formed by democratic process by a group of individuals or institutions or organization with a primary goal of saving their money to form a corpus that can be used for lending. The lending happens only for the members at a pre- agreed and fixed rate of interest.

The Credit Unions have the following features:

- they function in a democratic manner

- members are solely responsible for its functioning

- rate of interest charged are agreed upon mutually by the members

- they operate as not-for-profit financial cooperatives

- they are also known as saving and loan cooperatives

- they are not for profit financial union with every with members having a vote in the election of directors and committee representatives

- they act as self-regulatory organizations

4.3 Business Correspondent Model

The extent of financial inclusion in India is very low and there is vast scope of in the enhancement of financial inclusion. The planners do agree that lack of access to basic financial services is still a major challenge. The data suggests that more than 65% of the population in the country is either under banked or out of banking channels. To move forward in the direction of banking inclusion, RBI introduced a regulation in 2006 which allowed banks to provide service at people’s doorstep by utilizing third party services. This third-party intervention is known as Business Correspondents or Banking Correspondents’ (BC) model. In the past few years, banks are using their network of BCs to reach to new levels of financial servicing. The strategies towards improvement in the effectiveness of BC model have to be innovative for attracting new customer segments of economically poor people with low-income. Further, the model has to ensure diverse product range including client-oriented transactional accounts, remittance or payment services and suitable credit products. The utility of BCs is the fact that they have progressively moving towards operating like an extension counter of branches of banks. The objective is that after assuming functions of banks, regular banking products can be channeled through this model. The proposal of implementing social sector schemes

intervention/facilitation of any Non- Government Organisation (NGO). Model II - borrowers are financed directly with the facilitation extended by formal or informal agencies like Government, Commercial Banks and Micro-Finance Institutions (MFIs) like NGOs, Non-Bank Financial Intermediaries and Co-operative Societies; Model III - financing takes place through NGOs and MFIs as facilitators and financing agencies; Model IV - is the Grameen Bank Model, similar to the model followed in Bangladesh. In India, Model II of MF constitutes three- fourths of total micro-financing where activity/joint liability/Self-Help Groups are formed and nurtured by facilitating agencies and are linked directly with banks for the purpose of receiving credit [Arthapedia – a portal by government economists of India known as Indian Economic Services, http://www.arthapedia.in]. The literature survey shows that the approach adopted by different researchers and institutions have defined the various credit lending models prevalent differently. It can be further said that there is no consensus on the number of credit lending models because there are overlapping of features of these models and two or more models can have few features similar while other features can be divergent. This research to fulfill its objective of bringing all models on a single platform so that they can be studied together has primarily considered the features of these models as differentiating factor. The following paragraphs contains detailed discussion on various credit lending models which are in practice by various formal and non-formal institutions operating the domain of microfinance:

through the banking system with the support of Unique Identification (UID) provides enormous scope of BCs acting as intermediary between banks and clients. The banks have realized that their perspective of considering financial inclusion as a social activity rather than commercial proposition in fact was misplaced and this approach has on real time basis indirectly has led to increase in customer base or the deposits there by profits. RBI guidelines lays down the process of reaching out to any area by the bank with population greater than two thousand which becomes another barrier as such low numbers combined with minimal 8-10 transactions in kiosks and 30-40 transactions in Ultra Small Branches (USBs) per day makes this commercial banking non-profitable for the banks. There is an additional cap on the value of transactions not exceeding rupees ten thousand and amount of liquidity maintained at these branches has to be not more than rupees ten thousand leads to commercial banking becoming less scalable. The revenue generation remains low as the value of transactions are very less with an upper cap of Rs 12 / transaction while their operational expenses remain high which includes land rent, internet, electricity, operator salaries and other expenses. The infrastructure requirements Ultra Small Branches and Kiosks include fixed costs like basic needful technological gadgets which include computers, printers, photocopier, scanner, internet connections, LAN / Wi-Fi and other equipment. They are also required to buy biometric identification of employee for cash transactions. Thus, the cost of technological equipment can be considered high cost proposition by a bank’s branch. Hence, the role of intermediaries such as BCs and SHGs are considered to be very important for increasing the extent of financial inclusion in rural areas. Branch-based banking has high cost involvement therefore not an optimal option for serving customers at the bottom-of-the- pyramid. Thus, BCs have opportunity for the connect between banks and the customer.

However, BCs acceptance as a low-cost alternative channel is only just beginning to gain recognition among all the stakeholders. It is expected that revenues will take time to reach optimal levels for the operating banks as well as BCs. However, for reaching to the objective of financial inclusion, the outreach through BCs seems the only credible alternative on the horizon. Thus, focused efforts to rework at the financials and to adjust them so that BC model becomes viable propositions have to be worked out by planners and regulators. The stakeholders in financial inclusion in the country starts from common citizens, village influencers, RBI and Governments, NGOs, Institutional sources of credit at wholesale level viz. NABARD, RMK, SIDBI and sources of credit at retail level viz. commercial banks, Lead banks, RRBs and others, SHGs, The RBI and the government can provide policy directions and guidance however, the last mile of success hinges on banks to fulfill the goal of reaching out economic poor and financially excluded people. The BC model has the potential to act as a strong pillar for improving the last mile delivery. In spite of the fact that the BC model includes a number of financial services to the financially excluded people, the constraints that hinder the success of the model has reduced its efficiency. BCs are actually retail agents that are engaged by banks for providing banking services at locations other than a bank branch or ATMs. BCs enable a bank to provide its limited range of banking services at low cost. BC are authorized to offer services such as cash transactions in those places where the bank does have a branch. The main role of BC is to monitor the development and functioning of indirect banking channels. BCs remain under the RBI regulations and they maintain direct contact with one or more financial institutions. These BC’s are paid commission by the bank for enrollment of clients, transactions, deposits and other services.

BCs have to do a variety of functions viz, identification of borrowers, collection of small value deposit, disbursal of very small amount of credit, collection of repayments of both the principal amount and the interest amount, distribution of insurance products, mutual fund products, pension schemes. They also educate people about the financial products and services thereby increasing financial literacy. In the initial days after the launch of this scheme only ‘not for profit’ business entities were allowed to operate as BCs. Later on, the RBI allowed even business entities which were profit making firms to act as BCs. With more changes by the RBI, now the BCs are helping customers in rural areas access banking services such as cash deposits, withdrawals, remittances and balance enquiries from anywhere in the country on the lines of ATM facilities available to customers in urban areas. The BC model with passage of time is making significant progress in terms of coverage as well as value addition at lowest deciles of population in the economic pyramid. A number of participants have emerged, and several innovations were adopted in the banking system for facilitating the banking system to accept the BC model. However, there exists greater potential in terms of outreach and usage. Still, the sustainability of the model is one of the major concerns for both banks and BCs, which calls for in-depth understanding on the clients’ preference towards BC model. [Source: https://www.indianeconomy.net, 2016] RBI guidelines allows various products that can be offered by BCs. Few of these products are Small Savings Accounts, Term Deposits Recurring Deposit, Money Transfers, Microcredit, Insurance products, Microcredit, General Insurance. The BC model allows banks to provide door-step delivery of services especially cash transactions at a

location much closer to the rural population thus addressing the last-mile problem. The RBI guidelines have enlisted the list of entities both individual and institutional that can work as BCs.RBI has progressively modified to include registered entities like NGOs, MFIs. The list of entities was further modified, and new inclusions are individuals like retired bank employees, retired teachers, retired government employees and ex- servicemen, kirana shop owners, medical store owners, Fair Price distribution shops, Public Phone Centers, Insurance Agents, Financial Advisors of Mutual Funds, SHGs, Petrol Pumps and many more[Source: https://www.rbi.org.in/scripts/, 2014]. BC model adopted by banks are an extension of their branches with an outside arrangement towards expansion beyond their existing areas of operation. It is a new approach which is expected to become robust with passage of time, gaining operational experience. The current objective by and large has been to quantity financial inclusion in terms of processes and progression towards achievement of targets. In the focus of target achievement, the quality aspect has been ignored that further has resulted in not providing enough opportunity for the bank–BC partnership to develop and flourish. At this juncture, it is very much pertinent for the banks to ensure that BCs which are acting as vendors of financial service providers must be cost effective so that services can be rendered at lowest possible cost without comprising on the quality financial services. Banks need to adopt a wider perspective towards BC-bank relationship. It is needed because of two reasons – the focus has to change from compliance side of RBI directives regarding transactions towards profitability aspect of customer servicing. The second change in perspective needed is to legitimize the operations as BCs as an alternative channel of servicing the large segment of low- income people that may include the unbanked under banked people. The large number of people in this segment will enhance the financial viability of operations as

small pools of money will build a large corpus. This segment of people thereby will be a part of organized banking who are currently out of traditional banking and are usually denied access, convenience and quality service. The BC model is in the process of evolution and banks need to treat BCs as their extended arms of operation. It will lead to establishment of mutual trust and thereafter efforts to ensure win-win in the true spirit of partnership will gain ground. This will have wide level impact like segmenting customers, offering them suitable products addressing their needs, servicing them through the most efficient channels, investing in awareness building and focused marketing strategies. The banks can further identify those customers who can be serviced at their doorsteps. They can move the existing bank customers to the BC channel for door-step services. It will further lead to decongest branches and to provide improved service to their preferred customers. BCs will enhance their revenue because they operate on commission basis also, they will get assured customers. It will motivate them to offer superior service levels and to address customer expectations better. This model is However, still business correspondent network managers are struggling to get recognition at the ground level, and the viability of this channel is still not very much high. The BCs selection process has been adopted by banks under the direction of the Ministry of Finance. Bharat Microfinance quick Report – Microfinance growing Against All Odds (2012) by Sa-Dhan on the efficacy of Banking Correspondent model has identified that commercial viability is the greatest challenge because of low compensation paid to BCs which make model unsustainable. Another study by Micro Save conducted in Tamil Nadu, Uttar Pradesh and Rajasthan states reveals that over 80 per cent of India’s rural unbanked population is willing to pay for the convenience of banking at their doorstep through a banking correspondent. They feel it saves their time, energy and money in

travelling to and from the bank, waiting in the queue, improved security in cash handling, and the flexibility and convenience of BC model. Attracting the poor towards financial products such as recurring deposits, insurance premiums and mobile loan payments is a time-consuming process requiring patience and persuasive skills on the part of the bank staff or BCs. 4.3.1 Issues and Challenges faced by BC model This model faces serious challenges like lack of customer Service points, low morale and high expectations of BCs, poor selection process of BCs, exaggerated quantity features, low financial literacy support and no proper channel to address customer grievances. Among different models, Kiosk based model takes three-and-a-half years to break even under the best of circumstances whereas biometric GPRS mobile based model and SMS based remittance model takes about two years and less than two years respectively. The longer payback period on the investment made by BCs acts as a deterrent for entry of new players and raises questions on the sustainability of exiting entities. There are certain measures that need to be initiated for the sustainability of BC model:

- Financial stability needs to be provided to the BCs by funding the project requirement and assured minimum fixed income for few years will stabilized the BCs as viable entity.

- The RBI can formulate a range of uniformly applicable rates for the services provided by BCs.

- Members of SHG are also operating as BCs however they do not have rights to offer micro savings products. BCs and MFIs including NBFC-MFIs as BCs- NBFC-MFIs can offer saving products as BC.

- Channeling the payments made by governments to people through BCs. All payments to beneficiaries under government backed welfare programmes to be routed through BCs using the no-frill accounts.

- Banks needs to be paid a minimum of 2% of the payment value as operating and administrative expenses for effective management of BCs

- Integration of BCs with the national e- governance plan and Kiosk model of BCs to act as Common Service Centre

- There are many BC entities which are non-serious about the business they are carrying out. They need to be controlled and removed from the system

- The rural masses are not financial literate and many-a-times are not aware about the formalized banking channels and various financial services. Thus, financial literacy programmes needs to vigorously be pursued.

- In the entire landscape of BC Model, there is no grievance redressal mechanism hence a grievance redressal window will instill confidence among the customers.

- Diversification in the range of products offered coupled with quality services provided by BCs is the influencing factor for better revenue. BCs do have two important constraints – the liquidity issues and recurrent failure of technological platforms.

- Banks need to initiate programs related to necessary training and development of BCs staff. They need to realign product in-line with demand and offer a basket of products through BCs and make agent-banking a part of banks’ business strategies.

The All India Survey conducted by CGAP covering 860 sample Consumer Service Points (CSPs) in 11 states across the country to study the operational aspects of the CSPs operated under BC has concluded that BCs are yet to establish the economic sustainability with present remuneration level and mainly social relevance. It is only the enhanced reputation of BCs that is motivating them to continue in the business. The issues pointed out in the

CGAP survey can be resolved partly by the sponsoring banks by moving towards the solutions. However, the banks will be investing in the solutions only if they make financial inclusion forms a part of the core business of banks. The guidelines, which are in place as of now does not focuses much on financial inclusion as a part of core business of banks. Efforts needs to be made so that processes, procedures of the banks are integrated with the financial benefits thereby optimizing the business models at the ground level. The other part of the solution has to come from the regulator whereby RBI needs to give more attention to the nascent BC network and consider fixing its problems of viability, before expanding the same to smaller villages[Source: Microfinance India, State of the Sector Report, 2012] The BC model in spite its high potential of bringing about financial inclusion has not delivered effectively because of the embedded limitations within the model. The insights of the field visits show that their effectiveness is limited by the following concerns:

- a) Perspective of people towards bank branches A large section of people in India have perspective that the branches of banks will provide better guidance and safety of capital will be high. Thus, they are not very much keen in interacting with the BCs and they treat them as mere salesman.

- b) Expectation of BCs from banks are not fully met Banks have imposed high restrictions on operations of BCs regarding value of transactions and sale of financial products. Hence BCs feel constrained in meeting various demands of customers. While in reality, Jan Dhan Yojana relies heavily on the operations of BCs for continuation of account activities of the village people who started the account as part of the scheme. In short, the BCs expect more initiative and support from banks

- c) Low salary of BCs The salaries of BCs are very low as compared to the hard work they have to do to cover the distant areas.

- d) BCs are not interested in professional growth of career as BCs As per the current guidelines, the minimum qualification for BC is only secondary education (Class 10 th ). The younger BCs want to pursue their education and they look for better jobs as salary paid to them remains around 3500 to 4000 plus variable incentives. Hence most of the younger BCs look for better jobs elsewhere. Most of the BCs are not able to meet their family obligations with the salary that they get they do have alternative sources of income which reduces their interest in remaining BCs They feel that the BC is not permanent and growth opportunities are limited hence they attach very low value to the job.

- e) Failure of Banks to provide financial support for infrastructure creation. BCs expect financial support from the bank all the initiative for setting up kiosks comes from their own end with little support from the banks. BCs with investments on infrastructure face sustainability issues. Thus, the banks need to play larger role in taking appropriate measures for the progress in the development of financial inclusion in rural areas.

- f) Inappropriate people working as BCs A large section of BCs operating are retired employees and they lack interest in professional career. They want independence in their professional career and lack willingness to travel far and wide. Most of the BCs operating are retired schoolteachers.

- g) Low transactional values allowed for Ultra Small Branches PriortotheannouncementbythePrimeMinistero nAugust15, 2014, the maximum rupee value of transactions permissible for USBs was fixed at rupees five thousand and such a low transactional limit made it in convenient for customer and the bankers.

4.3.2 BCs as Facilitator of Swabhimaan Yojana of Government

Dedicated efforts are continuously being carried out by the financial institutions under the policy framework and supervision of the RBI and government through BC model. It is as an effective linkage between the banking network and the unreached clients. In 2010–12, the Swabhimaan campaign was launched by the government to extend a helping hand to improve banking facilities through BCs to all settlements with population more than 2000. In his budget speech 2012, the Union Finance Minister announced that out of 73,000 identified habitations that were covered in March 2012, about 70,000 have been provided with banking facilities. With this number over 25.5 million beneficiary accounts will be operating soon, the remaining will be covered by 31 March 2012. He further added that Ultra Small Branches will be set up at all those places and BCs will be empowered for cash transactions. In the year financial year 2012–13, the Swabhimaan campaign will be extended to cover all those settlements having a population of more than 1000 in the North Eastern and hilly regions and beyond where population has exceeded 2,000 considering the 2011 Census as basis. [https://pib.gov.in/newsite, 2020] and [Microfinance India: State of the Sector Report, 2014]

5.0 GROUP BASED MODELS

Various models are adopted by institutions for the disbursement of microfinance services in different parts of the world. The credit lending models can either be individual or group lending model. In individual lending models, credit is provided directly to the individual beneficiaries whereas group lending involves formation of a group and funds are provided to the group. In group- based credit lending models, the beneficiaries are group of people rather than individuals. The group lending models have common feature that they use peer pressure as a substitute of physical collateral. Individual

lending models are adopted by formal financial institutions like banks whereas group lending models are used by both MFIs as well as banks. The group lending and individual models have relative advantages and disadvantages. Table 1 given below illustrates few differences between these two models: requirements of any specific region. In fact, the group lending models are loosely related with each other in such a manner that the functionally effective and sustainable credit lending models have features of two or more models. It has been observed that functional credit lending models show high degree of overlap of features when put in practice. These credit lending models are the standardized and formalized models of local informal models operating outside the formal

here are many variants of group-based credit lending models. Few of the widely practiced group-based credit lending models are Association Model, Bank Guarantee Model, Community Banking Model, Grameen Joint Liability Group Model, Self-Help Group Model, Rotating Saving and Credit Association Model and Village Banking Model. In addition to these models there are few others like small business model, intermediaries’ model and NGO model. There can be local variations of these models suiting the socio-economic credit lending financial institutions. The evolution of credit lending has been unidirectional from informal channels to formalized financial institutions. The formal channels are ever increasing their outreach however, informal channels still

| Parameter | Individual lending | Group lending |

| Financial Institutions | Commercial banks, Money lenders | MFIs, Commercial banks, SHG, Bank-SHG linkages and others |

| Ease of transaction | Tedious paperwork for commercial banks and no paperwork for informal sources like moneylenders | Simplified procedure |

| Collateral Requirement | Collateral is required in most cases | Collateral is not required in most cases |

| Cost of Transaction per client | Transaction cost remains high | Transaction cost of group remains low and hence for individual it becomes even lower |

| Credit disbursement time | Credit disbursal happens after completion of tedious procedures of formal channels hence it takes more time however, in case of informal sources of individual credit, the disbursal is instant. | Credit disbursal time remains low as group itself acts as collateral |

| Requirement of staff | Generally, banks have more staff | MFIs operate with lower staff |

| Recovery process | Legal methods are used by formal institutions while coercive methods are used by informal sources. | The peer-pressure is the dominant method of recovery |

| Monitoring of usability of loans | In individual models, not much monitoring of loan usability is carried out | In group models, the group remains a cohesive unit thereby facilitating monitoring the members themselves |

| Financial education | Banks carry our financial education while information sources do not carry out any such activities | Financial education is a continuous and regular feature |

| Loan types | Loans are available only for production purposes from formal sources while there are no restrictions for the loans from informal sources | Loans are available for production and consumption purposes |

rather both these channels are co-existing in existence. Group-based credit lending models have different approaches to credit lending and cover the shortcomings and weaknesses of individual models. The weakness at the individual level are overcome by the sharing responsibility and security afforded by the formation of a group of such individuals. The voluntary joining of individual members to form group are used for a multitude of purposes like financial literacy promotion, creating awareness about benefits of microfinance, enhanced bargaining power and peer pressure, many more. Group models are more diverse in nature and it has influenced many other credit lending models. Few of them are Grameen, community banking, village banking, self-help, solidarity, peer pressure and others. For example, the Grameen model based on JLG has a typical feature that when a group receives credit all the members of JLG are jointly responsible for the repayment loan in case any of the members of the group defaults on the repayments.

5.1 Association Model

In the Association model, the target community’s members initiate and form an association. These group of individuals or associations are various center of microfinance activities. Associations Model is the primitive form of Group Models and various group models has its origin in this model. SHG model in India has evolved from Associations model. The compositions of this model are youths, men and women. They form around similar socio-religious-cultural groups. It often creates support systems and structures for micro enterprises. In many countries, an “association” turns to a legal entity which is entitled for complex microfinance functions like collection of fees, insurance, tax breaks and other protective measures. The most common activity of these associations is channelizing the micro-savings.

The associations look similar to NGO however, there is marked difference between these two in a way that associations are community- based groups which have all members and beneficiaries internal to the group while NGOs are always external organizations. Features of Association Model i. It is a form of group-based lending Model ii. Target community which shares common socio-religious and culture initiates and forms an association. iii. This model is the original version of SHG model iv. Members include: Youth and Women v. Source of funds: Internal as well as External funds

5.2 Community Banking Model

In this type of group-based lending model, the entire community is considered as a single unit. The understanding of entire community as one block leads to establishment of semi- formal or formal institutions through which microfinance services are dispensed. Such institutions are formed by extensive help from NGOs and other organizations, who also train the community members in various financial activities of the community bank. The community sets up its own bank which can be semi-formal or formal financial institution through which microfinance products and services are provided to the members of the community or customers of the Community Bank. It is a general practice that Community banks are formed and capacitated mostly by intermediaries like NGOs and other such organizations. The intermediaries operating in this segment adopts capacity building approach towards the community members and trains them in such a manner that they can discharge financial activities of the Community Bank. These institutions may have savings components and other income-generating projects included in their structure.

5.3 Bank Guarantee Model

This model has underlying feature that it provides a guarantee in a form of capital guarantee scheme. Bank’s guaranteed funds can be used for specified objectives which can be loan recovery and insurance claim. It has been efforts of international organization also to create an international guarantee funds that banks or the NGOs can subscribe for furthering the cause of providing microfinance services. This group-based credit lending model to a bank guarantee is used to obtain a loan from a commercial bank. The guarantee can be arranged either through an external source like donation from organizations or from government agencies. It can be arranged through internal sources in the form savings of the members. Funds acquired are directly credited to an individual or to a self-formed group.

5.4 Grameen Model Grameen

Model is an innovative model started by Prof Yunus in Bangladesh to bring about a change in quality of life the people at the bottom of the economic pyramid. The model focuses on economically poorer section of the society with no access to formal banking in order to augment their socio- economic status. Prof Yunus started Grameen bank in the rural areas of Bangladesh and the bank started operating as a poor centric grassroot institution providing microcredit to people who didn’t have access to any form of formal credit. Grameen model works on the fundamental that peer pressure acts as a form of collateral. The group members apply pressure for the repayment of loan that any member of the group has received. The collective responsibility of the group makes the repayment of loan nearly certain. Once the initial borrower repays the loan with interest, the loan facility is extended to other members of the group. Grameen model has provides the basic tenet of models like Grameen JLG model, Village banking model and Peer Pressure model.

5.4.1 Grameen JLG Model

Grameen JLG Model has originated from the Grameen Model started by Prof Yunus in Bangladesh. The Grameen JLG Model is the innovative outcome of the Grameen model. It came into existence through the operations of the Grameen bank at the grassroot level in Bangladesh. The Grameen JLG Model is considered as one of the most effective models in the disbursement of microfinance services in South East Asian region. The Grameen JLG model essentially works by setting up of a bank with a field managers and bank employees in rural areas comprising of 15 to 25 villages. The bank employees (field managers) start their activities by visiting villages to familiarize themselves with the villagers falling in their geographical areas of operation. The field managers explain their purpose, microfinance products on offer and modus operandi of the bank the villagers. The field managers form groups of five to seven prospective borrowers and one among them will receive the credit from the bank. The repayment of the group member is observed for a month to see if the members are conforming to rules of the bank. The Grameen Model works on the joint liability for the group members as an alternative to the physical collateral.

A detailed step wise operation of Grameen JLG is given below:

a) The field manager and their assistants develop acquaintance on working areas and thereafter build relationship with the target group or audience by paying regular visits to identified areas.

b) Field managers reveal the purpose, functions and operational model of the bank or MFI Making their intentions very clear to few people in village and model of credit. c) 5 - 7 prospective borrowers are identified and organized in a group called JLG.

d) Banking activity begins with provision of credit.

e) Only 2 of members can get credit out 5 -7 eligible members of the JLG.

f) After successful repayment in 6 – 15 weeks both principle and interest, the JLG is approved by the financial institutions.

g) Once it gets approved all the members become eligible for receiving the credit.

Advantage

a) Peer – pressures acts as collateral and hence repayment is nearly 100%. b) Since only 2 members can get loan, pear pressure forces them to repay.

c) Repayment is 100% nearly. d) Bank accounts and access to formal credit sources respectively.

5.4.2 Village Model Village

model has also evolved from Grameen model. They operate in rural areas and are basically community-based credit and savings associations. The members vary between 25 to 50 belonging to low-income strata in pursuit of improvement in the quality of their life through self-employment activities. The initial capital of these banks generally comes from external source. The capital received by the bank is managed by the members of the association. The officers of the bank are selected by democratic process. Once the employees are selected, they formulate operational guidelines and by-laws. The bank thereafter carries out banking services. This model also adopts the feature of Grameen Model that the joint liability for the group members as an alternative to the physical collateral. Few of the features of Village model resemble with the Community Banking and other features match with Group-based lending models.

5.4.3 Peer Pressure Model

Peer Pressure model is a part of Grameen model in way that it uses moral and other associations among borrowers and project participants to ensure participation and repayment of microfinance products and services. The members of the group are called Peers. In this model initial borrower has to repay both the principal and interest

component of the loan. Once the initial borrower repays the loan then only other members can receive loan. This results in peer pressure on the initial borrower to repay the loan. In this model an external NGO or bank identifies community leaders thereafter they are nurtured and trained. In peer pressure model, external agencies not only used peers to apply pressure additionally, they resort other methods like frequent visits to the defaulting member, organizing community meeting for requesting the member to repay the loan. Grameen model adopts peer pressure to ensure borrowers are following repayment schedule.

5.5 SHG Model SHG model in

India has evolved from the Grameen model of Bangladesh. The modified version of Grameen model i.e., Grameen JLG model is highly suitable for economically poor people living in densely populated areas where banking services are not available. However, in regions where population density is lower and banking network is adequate or high, Grameen JLG model may not remain effective in the same manner. The group- based credit lending model can be made effective in the regions where different geographical and socio-economic conditions prevail by modifying them to suit the local requirements. The modified version of Grameen JLG model used in regions of low population density and well banked regions is termed as SHG model.

Few of the features of SHG model are:

- Self-Sustainability SHGs are self-sustaining model because their source of funds primarily remains internal. They believe that self-help is best help and unity is strength.

- SHG-Bank Linkage SHGs remain linked with a bank and receive funds from the linked bank. The funds received are used for lending it to the members. The credit received by members is deployed in productive use. The productive use of funds by the SHG members not only enhances the timely repayment but also it leads to growth and expansion of the SHG and associated intermediaries.

- Capacity Building Approach SHG’s provides training for imparting skills to the members so that they can become self- reliant. The skill building approach leads to capability building among members and according to Dr Amartya Sen, developmental economist and Nobel laureate, the capability approach is way forward towards inclusive growth. Capability building approach of Dr Amartya Sen refers to activities of SHGs beyond lending operations. It refers to an approach in which SHG’s has secondary functions of conducting training session for its member’s, thereby building capability in them. As a result of capability building approach, the people at the bottom of economic pyramid are gainfully employed in fields like weaving, tailoring, handicrafts, carpentry and other similar activities additionally; they can also set up small entrepreneurial ventures.

- Participation of women The Grameen JLG model and SHG model have originated from Grameen model. However, SHGs have adopted a focused approach of disbursing loans only to female members. In general, SHGs members are mostly females while in JLF model members include male and females.

- Heterogeneity in composition of SHGs SHGs are heterogeneous in nature as far as its composition is concerned. The heterogeneity is in terms of Social, Religion and Culture of the members.

- Mode of Repayment of loan The most common mode of repayment of loan by the beneficiaries is cash to the SHGs or BCs in case of SHG-Bank Linkages

5.5.1 Shaping SHG

- Identification of group leader (CR)

- Conduction of regular meetings for

- revealing ideas

- dissemination of information related to government projects like Pradhan Mantri Jan Dhan Yojana, Pradhan Mantri Jeevan Jyoti Yojana, Atal Pension Yojana and others

Table2: Progress of SHG-Bank Linkage Programme in past few years

| Year | No. of SHGs with Savings Linkage | Amt of Savings outstanding | Total no SHG with extended loans | Amount of loan disbursed | No. of SHGs with loan outstanding | Amount of the loan outstanding |

| 2014 – 15 | 76.97 | 11.06 | 16.26 | 27.58 | 44.68 | 51.55 |

| 2015 – 16 | 79.03 | 13.69 | 18.32 | 37.29 | 46.73 | 57.12 |

| 2016 – 17 | 85.77 | 16.11 | 18.98 | 38.78 | 48.48 | 61.58 |

| 2017 -18 | 87.44 | 19.59 | 22.61 | 47.18 | 50.2 | 75.6 |

5.5.2 Methodology of SHG’s i.

In SHG model like Grameen JLGs, the field managers build rapport with the target audiences. They approach them through Sarpanches, School teacher and Gram Parishads. ii. Conduct of Baseline studies by SHGs regarding the profile of women. Baseline surveys are conducted to understand the socio economic and cultural characteristics of target audience by administering structured and unstructured questionnaire. iii. Groups are formed among SHG members having common mutual economic interest or similar skill sets or experience and having similar lifestyles. iv. Linkage of SHG with financial institution. SHG need to open an account with any bank in region in name of SHG. Loans are disbursed from MFI / bank.

5.5.3 Facilitation of SHG functioning i.

Regular discussions ii. Oath iii. Terms and Conditions

5.5.4 SHG – Bank Linkage Programme

This is bank-led microfinance channel introduced by NABARD in 1992 to facilitate economic enablement and financial inclusion for the bottom of the pyramid. SHG – Bank Linkage programme in last twenty-five years of

continuous journey has empowered the rural poor in general and rural women in particular.

| Evolution of model | It has directly emerged from Grameen model | It is Indian variant of Grameen model |

| Gender wise membership | Male as well as female members | Female members |

| Demographic feasibility | This model works best when people are homogenous | It remains independent of demographic profile of people |

| Geographical Requirement | This model is highly suitable in those regions where population density remains high | This model is suitable for areas where density of population remains low |

| Style of Governance | JLG are very rigid in nature | SHG are purely democratic in nature |

| Repayment responsibility and obligation | All the members are jointly responsible | The received of credit is only responsible |

| Eligibility criteria for credit | All members of JLG are not eligible for credit | All members are eligible |

| Effectiveness of model | JLG model is highly effective in those areas where banks do not have presence | SHG model is highly effective in regions which have network of banks |

| Current areas of operation | JLG model is popular in Bangladesh and South Africa | SHG model is widely used in India |

The linkage programme has now become the largest community-based microfinance initiative with 85.77 lakh SHGs as on March 31, 2017 covering more than a hundred million rural households [Microfinance Report, NABARD, 2017]. The table 9 shows the progress of SHG Banking Linkage programme. Under the SHG model the members, usually women in villages are encouraged to form

groups of around 15-20. The members pool their small savings as members of the SHG periodically and the corpus so aggregated through these savings is used to provide small loans to the members of the SHG. The banks through their SHG linkage programme provide loans to these SHGs generally for income generation purpose. The members of the SHGs conduct regular and periodic meetings. When the new savings come in, recovery of past loans are made from the members and also new loans are disbursed. This model is the most successful model among the group- based credit lending models and with passage of time the outreach is continuously increasing. The SHGs are self-sustaining and once the group becomes stable and it starts working on its own with some support from NGOs.

5.5.5 SHG Bank Linkage –Bank Account Requirements

Parameter JLG SHG

- SHG need to open a bank account

- Account in the name of SHG

- Loan disbursement from Bank / MFI

5.5.6 Comparison between SHG and JLG models (Table 3)

5.5.7 Benefits of SHG Model

SHG Bank Linkage programme started from 1992 has completed more than twenty-five years. In this period of over two decades the SHG bank linkages has emerged as an effective instrument of channeling scarce resources for the benefit of the poor and hence a vital tool for faster and inclusive growth. Within the concept of microfinance SHG-bank linkage programme has grown into such an effective model that not it is the world’s largest microfinance initiative. From linking a meager 500 SHGs representing non- banked rural poor to the formal sector institutions viz. commercial banks as a pilot project, SHG-BLP has now grown into 112 million families have been covered under SHG bank linkage programme with a total number of 85.77 lakhs SHGs with a saving amount of over 16000 crores. Around 50 lakhs SHGs have a total loan outstanding of over Rs 60 lakhs. In this period number of SHGs, which are linked to banks have witnessed high growth in the credit in the year 2017, [Sa- Dhan, The Bharat Microfinance Report, 2017]. 5.6 Intermediaries Model Intermediary model closely resembles the partnership model and NGO model. The features of this model have very high similarities with the features of NGO model. This model needs an individual or an organization which acts as go-between the

lending institution and the borrowers. The intermediary has an important task of creating awareness among borrowers about the benefits of credit through education, referring past cases, highlighting benefits of savings programmes. The efforts made are in the direction of enhancing credit worthiness of the borrowers to a level sufficient enough for the lending institutions to view them as attractive customers. The connect that the intermediaries make in the course of their operation are used for funding, programme links, training and education, and research. Such activities can take place at various levels from international and national to regional local and individual levels. The role of Intermediaries in this model is to act as a link between borrowers and the lending institutions and intermediary can be an individual, NGOs, Microenterprises and Commercial banks for government backed schemes. Lenders could be government agencies, commercial banks, international donors and others. Intermediary model becomes a part of various credit lending models that used in microfinance. Few of these models which uses intermediary model are BC model, NGO model, Association model etc. Most of these models mentioned do have some or other organizational or operational intermediary which deals directly with beneficiaries or for institutions dealing in microfinance services. 5.7 NGO Model NGOs are operating on various social- economic up upliftment programmes across the country. Many of the NGOs are promoting microfinance services among poor people. They have emerged as an effective intermediary between the people and financial institutions in the field of microcredit. NGOs remain active in microcredit programmes and facilitate smooth transaction between the financial institutions and the beneficiaries because of the reason that NGOs have higher

acceptability and trust among the poor people. The participation of NGOs in microcredit programmes can happen in many ways notable among them are creating awareness of the importance of microcredit among the members of the community in the geographically covered areas of its operation. The other contribution of NGOs in microcredit programmes is helping the people in completing KYC and other requirements of the credit disseminating bodies. NGOs also act as an interface between the various national and international donor agencies and the beneficiaries. NGOs do have experts who can give advice to the poor people. NGOs based upon their field operational experiences have devised techniques that can assess the progress of the work for which loan has been taken by the beneficiary. They also promote good practices among the society and have created opportunities to understand the principles and practice of microcredit through research, publications, workshops and seminars, symposiums, training programmes etc.

5.8 ROSCA Model

ROSCA is the acronym of Rotating Savings and Credit Associations. In ROSCA model group of individuals join their hands together to form an association and they make financial contributions at pre-determined periodicity. The corpus accumulated through these regular and uniform contributions are given to one of the members in lumpsum in each cycle of collection. The method ensures that each member receives the corpus of collected amount in every cycle of contribution made by members. In a typical ROSCA model, there are 10–15 members contributing rupees 1000 – 2000 every month. The corpus accumulated on monthly basis say 12000 – 24000 is given to one of members. The process continues till all the members get once the total corpus of one month. The principle behind is the fact that members provide credit to their fellow member. The member receiving the corpus repays the amount through regular

contributions. The decision the member who will receive the lump sum amount is done by consensus of members or using lottery method or any other commonly agreed methods.

5.9 Small Business Model

In the Small Business Model, microcredit is provided to entrepreneurs for starting small businesses. This model is in sync with the government policies which have focus on direct interventions for the enhancement of entrepreneurship culture through skill building, teaching, providing technical advice, management development programs and simultaneously creating good market environment for startups through policy initiatives. Skill India program is a comprehensive program launched on July 15, 2015 to train and develop entrepreneurial skills among Indians. The move to tap potential of India is unprecedented in the country’s history. Skill India has become a major project that involves every segment of the Indian society, local and foreign companies and governments. All the ministries of union government are directly or indirectly involved in the massive ‘Skill India’ program. This program is the world’s largest initiative in any country or any geographical location that involves training people for the achievement of self-employment. In India, MSME sector is emerging as a big driver of manufacturing sector. It has potential of creating jobs in large numbers. A high growth rate of the MSME sector will lead to enhancement of the economy thereby increasing formal jobs. The emphasis laid down in the Budget of 2019 on MSME is a direct outcome of cabinet committees’ decision to prioritize and seek solutions to two critical issues: creating new jobs and boosting investments. There are 63.38 million unincorporated non- farm MSMEs in the country engaged in different economic activities, including 19.66 million in manufacturing and 23 million in trade activities, according to data from the

MSME ministry. The sector employs more than 49.77 million people. As per the Economic Survey 2018-19, has put forth recommendation for incentivizing and handholding micro, small and medium enterprises (MSMEs) that are less than ten years of age, rather than providing benefits across the board. Given its focus on MSMEs, the government has also announced a pension scheme for 30 million small traders, recognizing the plight of shopkeepers, small traders and the self- employed hurt by the November 2016 decision to demonetize high-value currency notes, and the much-debated roll-out of the goods and services tax (GST) in July 2017. All small shopkeepers and self-employed persons as well as the retail traders with GST turnover below Rs1.5 crores and age between 18-40 years, can enroll for this scheme. The scheme would benefit more than 3 crores small shopkeepers and traders. [https://www.livemint.com, 2019]. With an aim of promoting MSME sector, the need of finance needs to be fulfilled specifically microcredit in different forms and for different uses. Microcredit has been provided to MSMEs directly, or as a part of a larger enterprise development programme in addition to skill building and other requirements.

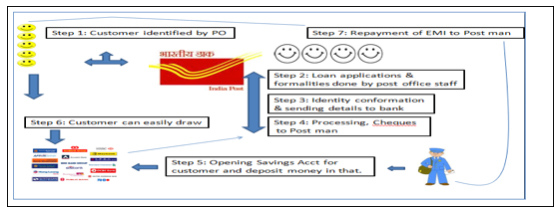

5.10 Post office Model

The various schemes that have been initiated by government and RBI have yielded positive results however financial inclusion is still a challenge considering the fact the more than fifty percent of the citizens are still financially excluded. The provision of financial services to unbanked people through various schemes has not been able to achieve the desired results of financial inclusion. It has happened because of the fact that many of these initiatives were entirely new schemes with little thought about synergy with other schemes existing in the system. The extent of financial exclusion in spite of presence of many financial institutions has forced the planners to look for a platform which has the potential of significantly increasing the extent of

financial inclusion. The much-needed platform for financial inclusion can be the post office. The post offices as a credit lending model can be highly effective because post offices had connected well with the society and they also provide financial services. The post office model believes that the existing extensive network of post office scan be leveraged by utilizing it as an alternative banking solution for the large sections of people who are still unbanked. In this context, existing banking facilities available for people at post offices have been explored and also their capabilities have been observed for the cause of financial inclusion at minimum cost and maximum synergies. India has the largest Postal Network in the world having 1.54 lakhs plus post offices and nearly 1.39 lakh (89.74%) are in rural areas. In comparison to the current number of post offices, at the time of independence, there were 23 thousand post offices, in the urban areas. The postal network has thus registered a seven-fold growth since independence with the focus of this expansion primarily being in the rural areas. The implementation of DARPAN Project with Core Banking Solution (CBS) will enable Department of Posts to roll out various social sector schemes on behalf of the Central and State governments through a network of 1.29 lakh Branch Post Offices in the rural areas. Rural Branch Post Offices will be provided with a Hand held Device enabled with biometric identification and Micro ATM functionality to perform various financial and postal transactions. Over 51 thousand branch post offices were a part of DARPAN Project by January 2018. [Source: Annual Report, Department of Posts, 2017-2018] The growth and outreach of post offices in rural areas can certainly act as an alternative mode of banking channel for the augmentation of financial inclusion.

5.10.1 Post Office – Grameen Bank Linkage model

The efforts made by central and state governments towards the financial inclusion of rural masses indeed have resulted in bringing rural people into the financial system. The schemes like Pradhan Mantri Jan Dhan Yojana have helped people in opening no frills accounts in banking thereby facilitating financial inclusion. The banks still find in economically difficult to serve rural areas through opening branches due to high establishment costs and relatively low deposit amounts. The banks and other financial institutions have tried BC model by using biometric devices. The advantages of BC model did have few advantages and it has been successful to some extent however, there are more unbanked people in India than the people covered by financial institutions. Post office model can be applied as an alternative model for financial inclusion because of its inherent strengths like deep penetration in rural areas and the trust that it enjoys among rural masses.

5.10.2 Post Office Model –

Key Deliverables Post office will enter into a tie-up with Grameen banks to set a new direction in the post office model.

The key deliverables can be:

- Post offices will work as an extension counter of banks for the collection deposits and other service requests on behalf of the banks

- Post offices can act as nodal center of financial services and act as business correspondent

- Post offices can act as centers for the disbursement of loans sanctioned by banks they can also accept re- payment through installments

5.10.3 Features of Post Office Model

The functioning of the post office model can broadly be classified into two categories viz. the collection of payment related procedures and disbursement related procedures:

(a) Collection of payments

- The Grameen bank and post offices can approach their existing customers and can tap the random footfalls in these institutions.

- The unbanked visitors can be educated regarding the benefits of bank account. The unbanked people need to be convinced for opening a bank account and necessary formalities has to be completed at the post offices itself. Post offices may collect the initial deposits of cash that the new customer wants to deposit.

- Post offices thereafter can send the completed form of the customer along with the payment made by the new customer through their cheque to the bank.

- In case of more than one deposit on any day, the cheque with the list of

- depositors and papers would be sent.

- Banks can open account in the name of the customer once the papers are in order. The passbook, cheque book and debit card have to be sent back to the post offices by the bank. The post offices in turn can handover these documents to the customer.

- In case of timed deposits, the customer will apply re-payment of investment amount in the post offices. The papers will be sent to the designated bank where from final sanction of the payment will be sent to the Postmaster who will make further the payment to the customer through the Savings Bank account.

Figure2: A hypothetical Post Office Bank Linkage Model

[Source:http://upost.gov.in/graminbank.html]

(b) Disbursement of payment related procedure

- The post offices will discuss the credit needs of their existing customers and people visiting the premises.

- The interested people will complete the formalities of loan disbursal at post offices.

- Thereafter, the post offices will forward all documents to the bank along with KYC documents.

- The bank after scrutinizing the papers will process the request and will send the cheque of amount of loan to the Postmaster. The Postmaster will open a Savings Bank Account of the customer and deposit the loan amount in that account. The customer can withdraw amount at his ease.

- Monthly re-payment EMI can be paid in the post offices in cash also. The post offices will forward the list of customers who have paid the installment amount to the bank through a single banker’s cheque.

- In case the re-payment is stopped, the Postmaster will provide the service of soft recovery by inquiring the reasons for non-payment and conveying it to the bank authorities.

- Account will be closed after last EMI is received. 5.10.4 Benefits of Post Office Model

- The post offices have deep penetration in the rural society and enjoy general trust of the public at large. The postmaster is considered as a person of wisdom and commands high respect in the rural society.

This trust can be leveraged out for the promotion of financial inclusion and rural people will the benefits like:

- Availing of banking services like deposit and withdrawals

- Credit facility and repayment of EMIs of loans

- Insurance schemes can be availed

- Government payments can directly get credited in their bank account

- Transparency in all financial transactions The post office Grameen bank linkage is not only beneficial for the rural people rather it offers many benefits for the Grameen bank.

Few of these banks are:

- Expansion of customer base through enhanced geographical coverage

- The recovery of loans will more effective due to presence of post

- offices as intermediary. It can happen because of the reason that postmaster remains well connected with the rural people than the bank manager.

- The banks will not be required maintain brick and mortar branch. It will lead to lowering of operational cost due to outsourcing of collection and disbursement services to post offices.

- The goodwill earned by the post offices in rural areas can be used for enhancement of financial literacy which in turn will lead to opening of accounts by the rural masses. In addition to the benefits that will accrue to the people as well as the Grameen bank, the post offices also stand benefitted from the linkage model.

The benefits that the post offices will derive are:

- There are many private companies that are handling mail services now-a-days popularly known as courier agencies. Hence post offices not the only medium of sending documents and they can diversify their business in newer areas.

- The technological platforms of transferring money like NEFT, IMPS, RTGS, UPI has reduced the volume of money orders hence post offices can re-deploy human capital in other financial services.

- The low rate of interest on NSCs and other such certificates have made them unattractive hence these qualified people can be used for handling post office Grameen bank linkage programme related activities.

- Post offices will be in a position to utilize its mass connect and trust that it enjoys among the rural people.

6.0 CONCLUSION